Implied Policy Rate Shifts

Fed is expected to cut today; the market believes it'll be by 50bps

The chart shows a comparison between the current implied policy rate curve (as of September 13, 2024) and a historical implied policy rate curve (as of June 13, 2024) for the United States (USD).

The implied policy rate is derived from market expectations of future central bank policy rates, typically using instruments like futures contracts.

Bloomberg Function: <MIPR>

Key Observations:

Downward Shift in the Implied Policy Rate Curve:

The green line (current implied policy rate) is lower across all tenors compared to the yellow line (historical implied policy rate), indicating that market now expects lower interest rates in the future than they did in June 2024.

Significant Drop Over Time:

The drop is especially notable over the 6-month and 1-year tenors, where the policy rate expectations have shifted downward by over 100 basis points (as shown in the lower red bars).

Possible Explanations:

Easing Inflationary Pressures: If inflation has begun to moderate or has come under control, the market may be anticipating that the central bank will slow or stop raising rates sooner than previously expected. This could explain the lower implied rates, especially in the medium-term tenors (6 months to 1 year).

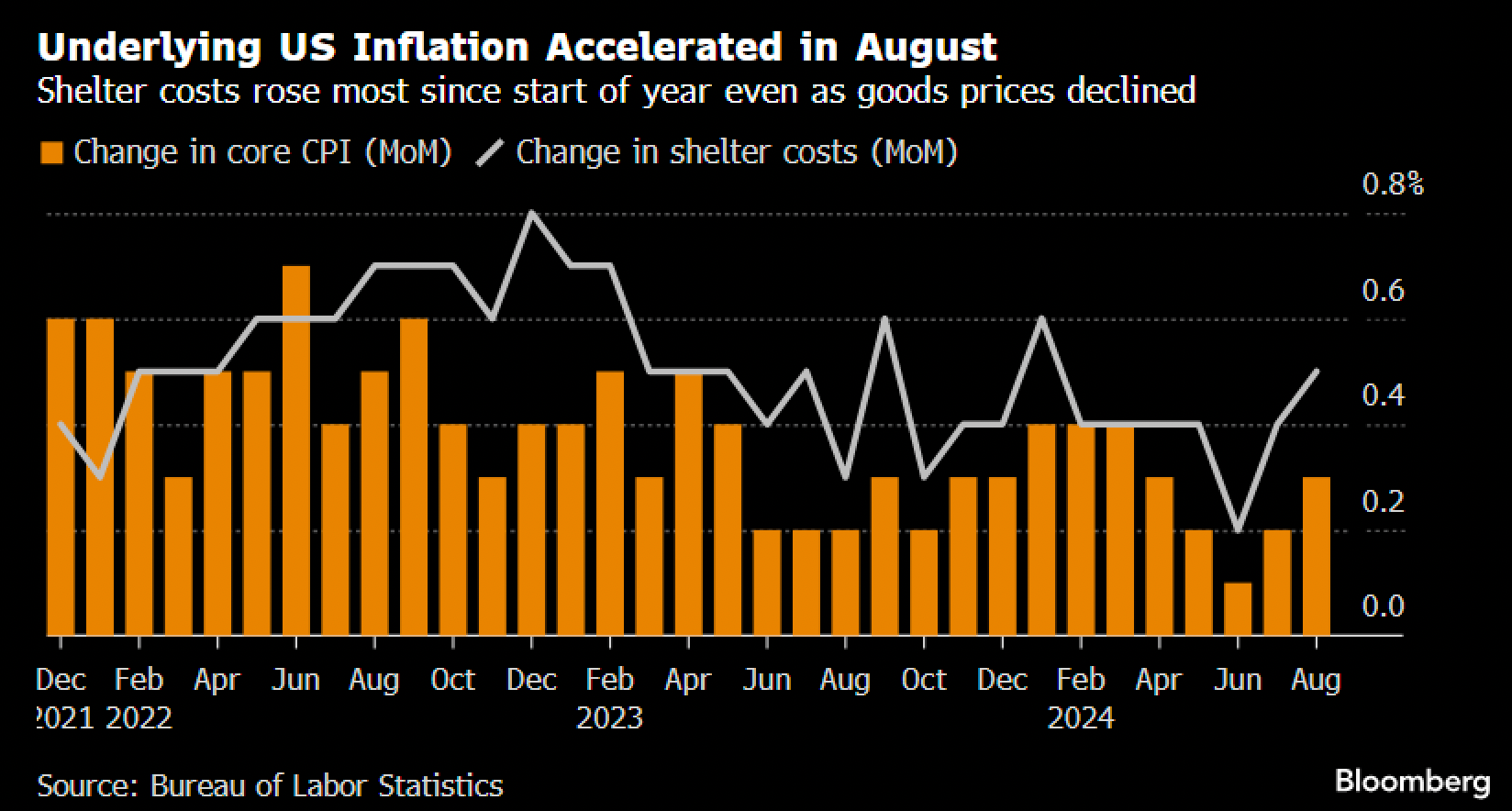

US core inflation picked up in August, reducing the likelihood of a large Federal Reserve rate cut in the near term, as the core Consumer Price Index (CPI) rose 0.3%, driven by shelter and travel costs.

However, while the unexpected rise in core U.S. inflation in August, driven by volatile components like lodging and airfares, dampened the likelihood of a larger 50-basis point rate cut at the Fed's next meeting, tilting expectations towards a more modest 25-basis point cut.

Economic Growth Concerns: A lowering of implied policy rates might also signal concerns about weakening economic growth or a potential recession. In such a scenario, the market may be pricing in future rate cuts as the central bank would likely lower rates to stimulate the economy.

To paint the picture that an economy is slowing, we should look at the following:

Gross Domestic Product (GDP) Growth Rate. Healthy, not slowing or contracting GDP.

Source: Bloomberg Unemployment Rate & Labor Market Trends. Unemployment is rising but not to levels that cause concerns.

Source: Bloomberg Beige Book showed: employment levels were generally flat to up slightly in recent weeks but layoffs remained rare. Wages rose at a modest pace.

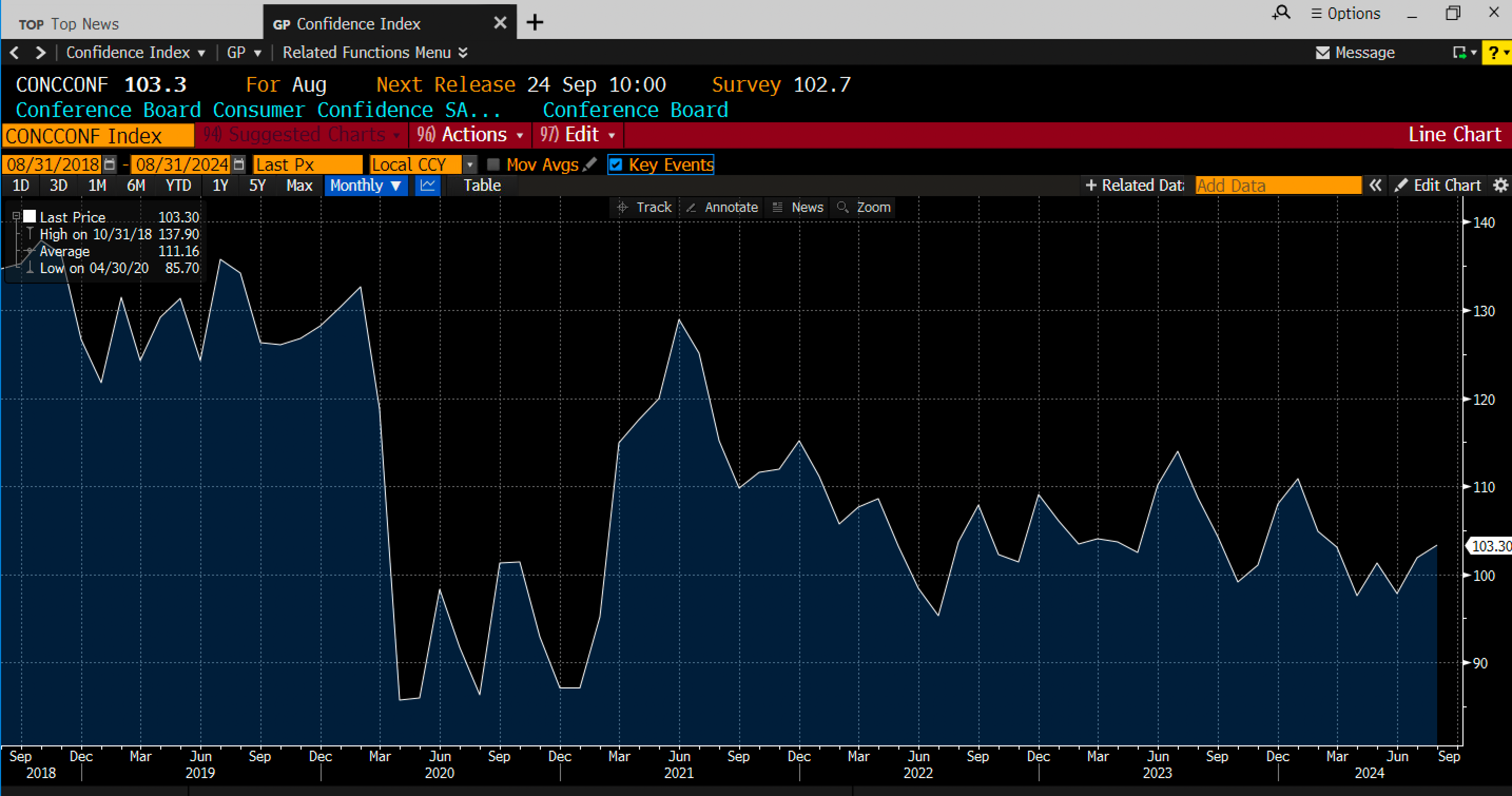

Consumer Spending. Reduced spending and consumer confidence. CONCCONF Index (Consumer Confidence)

Source: Bloomberg <ECST> (Key economic indicators) You can filter for

Personal Consumption Expenditures (PCE).

Retail Sales (monthly data is available for retail sales).

Personal Income and Outlays (provides deeper insights into household spending and saving behaviors).

Business Investment (Capital Expenditures). Falling capital expenditures and weak business sentiment?

Inflation (<IFMO>) & Wages. Declining inflation, stagnant wages, or businesses facing margin pressures?

End of Tightening Cycle: The steep decline over the short-term tenors (1 to 6 months) may suggest that market participants believe the current rate “pause” cycle is ending, with expectations of rate cuts in the medium term.

Changes in Monetary Policy Expectations: The Federal Reserve have hinted at a more dovish stance due to new economic data, leading markets to adjust expectations for a less aggressive policy path. This would lead to a shift downward in the implied policy rate across all tenors.

Powell, speaking Friday 23 August 2024 at the US central bank’s annual symposium in Wyoming, said the “time has come” for the Fed to lower benchmark rates from their two-decade high, his clearest signal yet that long-awaited rate cuts are imminent.

Trades/Investments that benefit this shift:

1. Long Duration Bonds

Rationale: You are betting that interest rates will fall across all maturities, which increases the price of long-term bonds more significantly (due to higher duration sensitivity).

Trade Idea: Buy U.S. Treasuries with longer maturities (e.g., 10-year, 30-year) or corporate bonds with long duration. You could also consider ETFs that focus on long-duration fixed income securities.

Also note that if an FI investment manager is long duration, they believe that interest rates are decreasing.

Success in Prolonged Rate-Cutting Cycles: When the Fed has entered sustained periods of monetary easing (e.g., during and after recessions), long duration bonds have typically performed well. This is because as the Fed cuts rates, yields fall, and the price of long-term bonds rises significantly due to their higher duration sensitivity.

For example:

2008 Financial Crisis: Long-term U.S. Treasuries performed exceptionally well as the Fed aggressively cut rates to near zero. Investors flocked to safe assets, and long bonds saw significant price appreciation.

COVID-19 Pandemic (2020): Similarly, during the 2020 pandemic-induced recession, the Fed slashed rates, and long-duration bonds rallied as yields plummeted across the curve.

2. Receive Fixed in Interest Rate Swaps

Rationale: In an interest rate swap, receiving the fixed rate while paying the floating rate would benefit from the anticipated fall in rates.

Trade Idea: Enter into an interest rate swap where you receive the fixed rate and pay the floating rate, locking in today's higher rates before they fall.

3. Steepener Trades (*)

Rationale: You are betting that short-term rates will fall faster than long-term rates, causing the yield curve to steepen. This trade involves a relative bet between short-term and long-term yields.

Trade Idea: Go long on short-term bonds (benefiting from falling short-term rates) and short long-term bonds, or use interest rate futures to implement a steepener position.

Steepener Trade is Successful in Early Stages of Rate Cuts or "Soft Landings": Steepener trades tend to perform better in the early stages of rate-cutting cycles, particularly when the market expects short-term rates to drop faster than long-term rates, often due to the Fed trying to engineer a "soft landing" without pushing long-term rates lower.

For example:

1990s Soft Landing: During the Fed's soft landing in the mid-1990s, the steepener trade worked well as short-term rates fell faster than long-term rates, steepening the yield curve.

Early 2000s: In the early 2000s, during the dot-com crash, the steepener trade worked as the Fed cut short-term rates aggressively to combat the downturn, while long-term rates stayed relatively steady, leading to a steepened curve.

4. Equities in Interest Rate-Sensitive Sectors

Rationale: Lower interest rates tend to benefit sectors like utilities, real estate, and consumer discretionary, as lower borrowing costs improve profitability for these capital-intensive sectors.

Trade Idea: Go long on equities in sectors that are sensitive to interest rates, such as utilities, REITs (Real Estate Investment Trusts), or consumer discretionary stocks.

5. Refinancing and Mortgage-Backed Securities (MBS)

Rationale: Lower interest rates often lead to increased refinancing activity in the housing market, benefiting mortgage-backed securities.

Trade Idea: Consider MBS or ETFs that focus on mortgage-backed securities. However, be cautious of prepayment risk, as lower rates may cause more prepayments and early retirements of the underlying loans.

6. Currency Trades (USD Short)

Rationale: If U.S. interest rates are expected to fall while rates in other countries remain stable or rise, the U.S. dollar may weaken against other currencies.

Trade Idea: Short the U.S. dollar (USD) against currencies of countries with stronger or more stable interest rate outlooks, such as the XXXX or Japanese yen (JPY).

7. Gold and Commodities

Rationale: Lower interest rates can weaken the dollar and increase demand for commodities like gold, which often moves inversely to the dollar and is seen as a store of value in low-rate environments.

Trade Idea: Go long on gold or other commodities that tend to benefit from a lower interest rate environment.

8. Leverage and Credit Trades

Rationale: Lower interest rates reduce the cost of borrowing, potentially increasing corporate leverage or driving up demand for high-yield credit.

Trade Idea: Invest in high-yield corporate bonds or leveraged loans, as companies take advantage of the lower rates to finance expansion or refinance existing debt.

9. Call Options on Equities

Rationale: Lower interest rates are generally bullish for equity markets, especially when borrowing costs are lower and economic activity might get a boost.

Trade Idea: Buy call options on broad equity indices (e.g., S&P 500) or rate-sensitive sectors that could rise as rates drop.

Trades/Investments if contrarian:

I personally believe that the market is too dovish. Here’s a list of potential trades if contrarian view to that implied by the market.

Ray Dalio believes it should be 25 bps if looking at the economy as a whole, or 50bps if looking at mortgage-holder. “The Fed has to keep interest rates high enough to satisfy the creditors that they are going to get a real return without having them so high that the debtors have a problem,”

1. Sell Duration (Short Bonds)

Rationale: If rates fall more slowly than expected, bond yields will remain higher than currently priced in, which would cause bond prices to decline.

Trade Idea: Short long-duration U.S. Treasuries, such as the 10-year or 30-year bonds, or use futures to short bonds. If rates don't fall as much as implied, you would profit from the bond prices falling (or not rising as much as expected).

2. Pay Fixed in Interest Rate Swaps

Rationale: By paying the fixed rate and receiving the floating rate in an interest rate swap, you are essentially betting that future rates will not decline as much as the market expects.

Trade Idea: Enter into an interest rate swap where you pay the fixed rate and receive the floating rate. If the actual rate cuts are slower or smaller than expected, you benefit because the floating rate would not drop as much as the market currently predicts.

3. Steepener Trade (Short Front End, Long Back End)

Rationale: If the Fed reduces rates more slowly than expected, short-term rates (front end) would stay elevated longer, while long-term rates (back end) may reflect eventual easing. This would steepen the yield curve.

Trade Idea: You could enter into a yield curve steepener by shorting short-term bonds (2-year U.S. Treasuries) and going long on longer-term bonds (10-year U.S. Treasuries). If the Fed lowers rates more slowly, the front-end of the curve will stay higher, and you will profit from the widening yield spread.

4. Short Federal Funds Futures

Rationale: Federal funds futures are often used to gauge market expectations of interest rate moves. If you believe the Fed will lower rates at a slower pace than implied, these contracts are likely overestimating the amount of rate cuts.

Trade Idea: Short federal funds futures contracts that are pricing in larger rate cuts than you expect. If the actual rate cuts are smaller or delayed, these futures would decline in value, and you would profit from your short position.

5. Sell Eurodollar Futures

Rationale: Eurodollar futures, which are based on the U.S. dollar-denominated deposits held outside the U.S., are also highly sensitive to expectations of U.S. interest rates. If you expect slower Fed cuts, Eurodollar futures, which currently imply faster or deeper cuts, could fall in price.

Trade Idea: Short Eurodollar futures, especially contracts for the next 12-24 months that are pricing in aggressive rate cuts. If rate cuts happen slower than expected, these contracts will decline in value.

6. Long U.S. Dollar (USD)

Rationale: If the Fed is expected to cut rates more slowly than anticipated, U.S. interest rates will remain relatively high, making U.S. assets more attractive, which could support the U.S. dollar.

Trade Idea: Take a long position in the U.S. dollar (USD) against other currencies, especially those where central banks are cutting rates faster (e.g., EUR or JPY). A slower rate-cutting cycle in the U.S. should support the dollar relative to other currencies.

7. Short High-Growth Equities or Rate-Sensitive Sectors

Rationale: High-growth stocks and interest-rate-sensitive sectors (like real estate or utilities) tend to rally when rates are expected to fall sharply. If the Fed slows the pace of rate cuts, these sectors may underperform.

Trade Idea: Short high-growth stocks or ETFs focused on rate-sensitive sectors (e.g., utilities, REITs) that have rallied on expectations of significant rate cuts. These sectors may correct if rate cuts are slower than expected.

8. Credit Spread Widening (Short Corporate Bonds)

Rationale: Slower-than-expected rate cuts could keep borrowing costs higher for longer, putting pressure on corporate borrowers, especially in high-yield or speculative-grade credit.

Trade Idea: Short high-yield corporate bonds (e.g., via ETFs like HYG or JNK) or buy credit default swaps (CDS) on companies that might struggle with higher borrowing costs. Corporate spreads may widen if rates stay elevated longer than expected.